Are you shopping in Asheville’s higher price ranges and wondering if your loan will be considered “jumbo”? You are not alone. Between unique mountain properties, varying lender rules, and shifting market conditions, it can be hard to know what to expect. In this guide, you will learn how jumbo loans work, where the limits sit, what is different in Asheville, and the steps to prepare a strong application. Let’s dive in.

Jumbo loan basics

A jumbo mortgage is any loan amount that exceeds the conforming loan limit set by the Federal Housing Finance Agency (FHFA). Conforming loans can be purchased by Fannie Mae and Freddie Mac, while jumbo loans are typically held by lenders or sold in private markets. Because of that difference, jumbo loans usually come with tighter credit standards and more documentation.

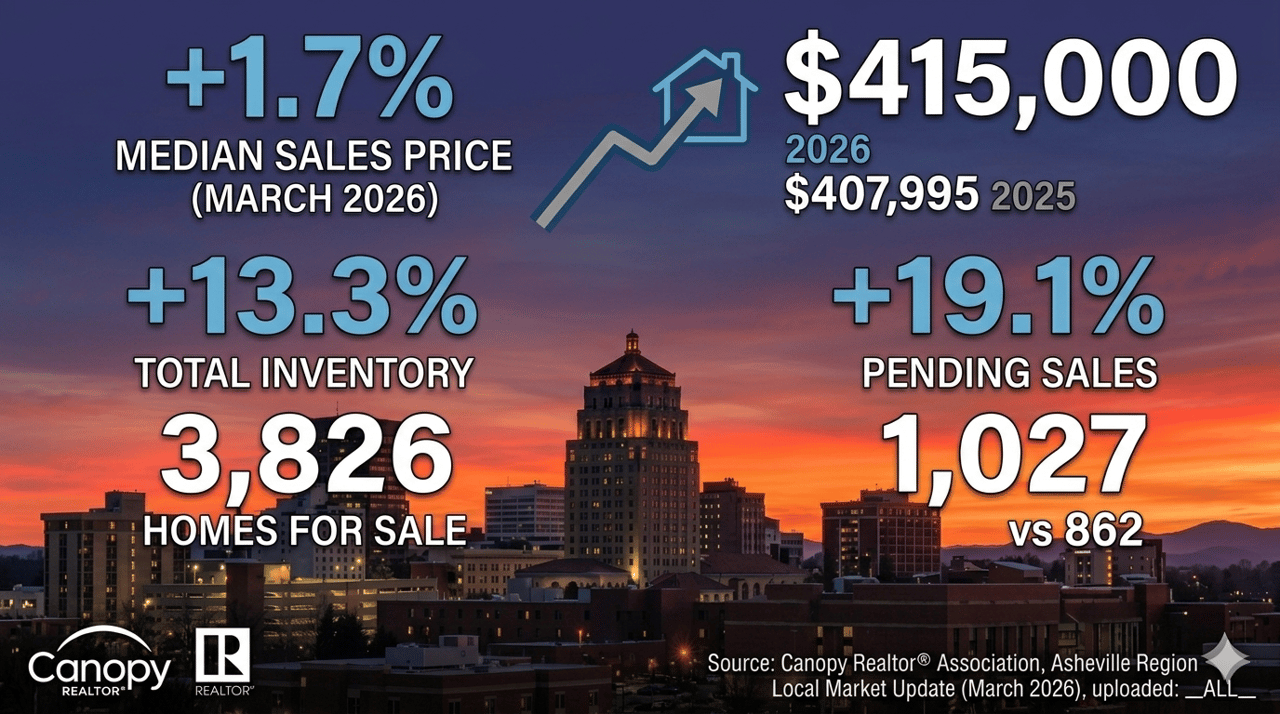

For 2024, the national baseline single-family conforming loan limit is $766,550. Whether a specific purchase in Buncombe County is considered jumbo depends on the current year’s FHFA limit and any county-specific designation. Limits can change each year, so verify the latest figure when you start your search.

Where Asheville buyers encounter jumbo

In Asheville and across Buncombe County, jumbo loans are common for luxury homes, properties with extensive views or acreage, and unique or historic residences. Out-of-area demand and second-home buying can also push prices into jumbo territory. If your target list includes high-end neighborhoods or distinctive mountain properties, plan for jumbo-level underwriting.

How jumbo underwriting differs

Credit and income

- Lenders often want higher credit scores, with the most competitive pricing typically at 740 and above.

- Debt-to-income ratios are scrutinized more closely, though strong compensating factors like large reserves can help.

Down payment and reserves

- Expect minimum down payments in the 10 to 20 percent range, with many borrowers choosing 20 percent or more for better pricing.

- Cash reserves after closing are common, often 6 to 12 months of total housing payments, especially as loan amounts rise.

Documentation and appraisal

- Be prepared for more extensive documentation: tax returns, bank and investment statements, employment and income verification, and explanations for large deposits.

- Appraisals on mountain or unique properties may require specialized local expertise and, at times, a second opinion.

Rates and products

- Rate spreads between jumbo and conforming loans change over time. Sometimes the gap is small; at other times it widens.

- You will find both fixed and adjustable-rate jumbo options, plus some non-QM choices for self-employed buyers or those with complex finances.

Asheville-specific factors to plan for

Property access and topography

Mountain access, steep driveways, and private roads are common outside city centers. Lenders may ask for road maintenance agreements or additional documentation. Plan for extra time to gather these items.

Septic, wells, and utilities

Homes outside town often use septic systems and well water. Lenders can require inspection reports, capacity details, and permits. Confirm system information early to avoid delays.

Short-term rental considerations

If you are buying with short-term rental expectations, know that lenders treat STRs as investment properties. Underwriting is stricter, with higher down payment and reserve requirements and close review of local rules and HOA policies.

Condos and HOAs

Condo projects must meet lender eligibility standards. Smaller or boutique buildings can face added scrutiny, so expect questions about budgets, insurance, litigation, and owner-occupancy ratios.

Taxes, insurance, and flood zones

Property taxes and any floodplain designations affect your monthly costs and insurance. Verify tax records and check flood zone status early in due diligence so your lender and insurer can price the risk correctly.

Steps to get jumbo-ready in Asheville

- Get preapproved with at least two lenders who regularly originate jumbo loans in the Asheville area.

- Strengthen your credit profile and reduce revolving debt where possible to improve pricing and approval odds.

- Build your documentation package in advance and keep it organized. Expect follow-up requests during underwriting.

- Discuss appraisal and inspection timelines with your agent and lender, especially for unique homes or rural parcels.

- Consider a lender or broker familiar with mountain properties and local appraisers to keep the process moving.

Document checklist

- Photo ID and Social Security number

- Most recent 2 years of federal tax returns, plus K-1s if applicable

- Recent pay stubs covering 30 days and W-2s for the past 2 years

- Business tax returns and profit/loss statements if self-employed

- 2 to 3 months of bank and investment statements; include retirement accounts if relevant to qualifying

- Gift letter if using gifted funds for the down payment

- Explanations for large deposits or recent credit inquiries

Timeline and rate locks

Jumbo underwriting can take longer than conforming financing. Unique property appraisals and added documentation reviews can extend the process. Ask about rate lock options and any fees for longer locks so you can protect your rate if timelines shift.

Second homes, investments, and VA considerations

Jumbo financing is available for second homes and investment properties, but expect stricter standards. You may face higher down payments, more reserves, and additional documentation on local approvals for rentals. VA borrowers with full entitlement are not limited by statutory loan caps, but individual lenders still set overlays and reserve requirements for high-balance VA loans.

Common pitfalls to avoid

- Not verifying private road maintenance or shared driveway agreements.

- Underestimating the time and documentation needed for well, septic, or special-use inspections.

- Assuming a condo is financeable without checking project eligibility and HOA documents.

- Relying on future short-term rental income without confirming local allowances and lender requirements.

Your path forward

If you are targeting a distinctive mountain home or a luxury property in Buncombe County, planning for jumbo financing early will keep your purchase on track. With the right preparation, team, and timeline, you can move from offer to close with fewer surprises. If you want a clear path and local guidance tailored to Asheville’s market, reach out to Preston Mayfield. Let’s connect.

FAQs

What counts as a jumbo loan in Buncombe County?

- Any mortgage above the current FHFA conforming loan limit for single-family homes is jumbo. For 2024, the national baseline is $766,550; verify the current year when you apply.

How much down payment do Asheville jumbo buyers need?

- Many lenders require 10 to 20 percent down, and 20 percent or more often brings better pricing and fewer overlays.

Are jumbo mortgage rates always higher?

- Not always. The spread between jumbo and conforming rates changes with market conditions and lender competition.

What extra documents will lenders ask for on a jumbo?

- Expect full tax returns, bank and investment statements, employment and income verification, and explanations for large deposits or credit inquiries.

How do Asheville’s mountain properties affect appraisals?

- Unique homes, views, acreage, and rural locations can make comparable sales harder to find, which may lengthen appraisal reviews or trigger a second opinion.

Can I use a jumbo loan for a second home or STR?

- Yes, but underwriting is stricter. Plan for higher down payments, more reserves, and documentation of local rental rules and any HOA restrictions.

Do VA borrowers have a jumbo limit in Asheville?

- Borrowers with full VA entitlement are not capped by statutory loan limits, but lenders set their own overlays and reserve requirements for high-balance VA loans.